OVERVIEW OF MARINE INSURANCE

What is Marine Insurance?

According to the Insurance Code of the Philippines, marine insurance includes:

(a) Insurance against loss of or damage to:

(1) Vessels, craft, aircraft, vehicles, goods, freights, cargoes, merchandise, effects, disbursements, profits, moneys, securities, choses in action, instruments of debts, valuable papers, bottomry, and respondentia interests and all other kinds of property and interests therein, in respect to, appertaining to or in connection with any and all risks or perils of navigation, transit or transportation, or while being assembled, packed, crated, baled, compressed or similarly prepared for shipment or while awaiting shipment, or during any delays, storage, transhipment, or reshipment incident thereto, including war risks, marine builder’s risks, and all personal property floater risks;

(2) Person or property in connection with or appertaining to a marine, inland marine, transit or transportation insurance, including liability for loss of or damage arising out of or in connection with the construction, repair, operation, maintenance or use of the subject matter of such insurance (but not including life insurance or surety bonds nor insurance against loss by reason of bodily injury to any person arising out of ownership, maintenance, or use of automobiles);

(3) Precious stones, jewels, jewelry, precious metals, whether in course of transportation or otherwise; and

(4) Bridges, tunnels and other instrumentalities of transportation and communication (excluding buildings, their furniture and furnishings, fixed contents and supplies held in storage); piers, wharves, docks and slips, and other aids to navigation and transportation, including dry docks and marine railways, dams and appurtenant facilities for the control of waterways.

(b) Marine protection and indemnity insurance, meaning insurance against, or against legal liability of the insured for loss, damage, or expense incident to ownership, operation, chartering, maintenance, use, repair, or construction of any vessel, craft or instrumentality in use of ocean or inland waterways, including liability of the insured for personal injury, illness or death or for loss of or damage to the property of another person. (Section 101 Insurance Code of the Philippines)

On the other hand, according to Marine Insurance Act of England, it is defined as:

A contract whereby the insurer undertakes to indemnify the assured, in manner and to the extent thereby agreed, against marine losses, that is to say, the losses incident to marine adventure. (Section 1, Marine Insurance Act of England 1906)

There is a marine adventure where -

What are the types of Marine Insurance according to risk covered?

What are the kinds of Marine Insurance according to type of policy?

They are as follows:

According to the Insurance Code of the Philippines, marine insurance includes:

(a) Insurance against loss of or damage to:

(1) Vessels, craft, aircraft, vehicles, goods, freights, cargoes, merchandise, effects, disbursements, profits, moneys, securities, choses in action, instruments of debts, valuable papers, bottomry, and respondentia interests and all other kinds of property and interests therein, in respect to, appertaining to or in connection with any and all risks or perils of navigation, transit or transportation, or while being assembled, packed, crated, baled, compressed or similarly prepared for shipment or while awaiting shipment, or during any delays, storage, transhipment, or reshipment incident thereto, including war risks, marine builder’s risks, and all personal property floater risks;

(2) Person or property in connection with or appertaining to a marine, inland marine, transit or transportation insurance, including liability for loss of or damage arising out of or in connection with the construction, repair, operation, maintenance or use of the subject matter of such insurance (but not including life insurance or surety bonds nor insurance against loss by reason of bodily injury to any person arising out of ownership, maintenance, or use of automobiles);

(3) Precious stones, jewels, jewelry, precious metals, whether in course of transportation or otherwise; and

(4) Bridges, tunnels and other instrumentalities of transportation and communication (excluding buildings, their furniture and furnishings, fixed contents and supplies held in storage); piers, wharves, docks and slips, and other aids to navigation and transportation, including dry docks and marine railways, dams and appurtenant facilities for the control of waterways.

(b) Marine protection and indemnity insurance, meaning insurance against, or against legal liability of the insured for loss, damage, or expense incident to ownership, operation, chartering, maintenance, use, repair, or construction of any vessel, craft or instrumentality in use of ocean or inland waterways, including liability of the insured for personal injury, illness or death or for loss of or damage to the property of another person. (Section 101 Insurance Code of the Philippines)

On the other hand, according to Marine Insurance Act of England, it is defined as:

A contract whereby the insurer undertakes to indemnify the assured, in manner and to the extent thereby agreed, against marine losses, that is to say, the losses incident to marine adventure. (Section 1, Marine Insurance Act of England 1906)

There is a marine adventure where -

- Any ship goods or other movables are exposed to maritime perils. Such property is in this Act referred to as “insurable property”;

- The earning or acquisition of any freight, passage money, commission, profit, or other pecuniary benefit, or the security for any advances, loan, or disbursements, is endangered by the exposure of insurable property to maritime perils;

- Any liability to a third party may be incurred by the owner of, or other person interested in or responsible for, insurable property, by reason of maritime perils

- “Maritime perils” means the perils consequent on, or incidental to, the navigation of the sea, that is to say, perils of the seas, fire, war perils, pirates, rovers, thieves, captures, seizures, restraints, and detainments of princes and peoples, jettisons, barratry, and any other perils, either of the like kind or which may be designated by the policy. (Section 3, Marine Insurance Act of England 1906)

What are the types of Marine Insurance according to risk covered?

- Marine Cargo Insurance - covers loss or damage to insured goods while in transit, whether on land, sea or air.

- Hull Insurance - covers loss or damage to the vessel's hull, machinery and equipment, including collision liability.

- Stock Throughput Insurance (STP) - cover loss or damage to insured goods from production and to the final destination. It shall cover different modes of transportation such as ocean, air and inland transit. Such cover is in addition to storage and periods in warehouses at each production stage.

- Liability Insurance - covers liability by those engaged in the shipping industry. Examples of this class of insurance are:

- Ship Repairers Liability Insurance

- Port Operator's Liability Insurance

- Charter's Liability Insurance

- Protection & Indemnity (P&I) Insurance - protects shipowners from the maritime liability risks associated with owning and operating a vessel.

What are the kinds of Marine Insurance according to type of policy?

They are as follows:

- Voyage Policy - a policy that covers a single voyage only.

- Open Policy - a policy whereby the insurer agrees to provide coverage for all cargo shipped by the insured during the policy period.

What are the implied warranties in Marine Insurance? (2000 Bar Exams)

They are as follows:

Define seaworthiness and when is a ship deemed seaworthy?

A ship is seaworthy when reasonably fit to perform the service and to encounter the ordinary perils of the voyage contemplated by the parties to the policy.

An implied warranty of seaworthiness is complied with if the ship be seaworthy at the time of the commencement of the risk, except in the following cases:

When is deviation deemed proper?

It is deemed proper if the following are present:

Is the warranty of seaworthiness applicable to the cargo owner too aside from the shipowner?

Since the law provides for an implied warranty of seaworthiness in every contract of ordinary marine insurance, it becomes the obligation of a cargo owner to look for a reliable common carrier which keeps its vessels in seaworthy condition. The shipper of cargo may have no control over the vessel but he has full control in the choice of the common carrier that will transport his goods. (Isabela Roque vs Intermediate Appellate Court and Pioneer Insurance and Surety Corporation, (G.R. No. L-66935 November 11, 1985)

Who are the parties in the Marine Adventure?

What is a common carrier?

Common carriers are persons, corporations, firms or associations engaged in the business of carrying or transporting passengers or goods or both, by land, water, or air, for compensation, offering their services to the public.

Common carriers, from the nature of their business and for reasons of public policy, are bound to observe extraordinary diligence in the vigilance over the goods and for the safety of the passengers transported by them, according to all the circumstances of each case.

What is the test for determining whether a party is a common carrier of goods or not?

The following elements must be satisfied:

Will the fact that petitioner has a limited clientele does not exclude it from the definition of a common carrier?

Art. 1732 of the Civil Code makes no distinction between one whose principal business activity is the carrying of persons or goods or both, and one who does such carrying only as an ancillary activity (in local idiom, as a "sideline"). Article 1732 . . . avoids making any distinction between a person or enterprise offering transportation service on a regular or scheduled basis and one offering such service on an occasional, episodic or unscheduled basis. Neither does Article 1732 distinguish between a carrier offering its services to the "general public," i.e., the general community or population, and one who offers services or solicits business only from a narrow segment of the general population. We think that Article 1877 deliberately refrained from making such distinctions.

The concept of "common carrier" under Article 1732 may be seen to coincide neatly with the notion of "public service," under the Public Service Act (Commonwealth Act No. 1416, as amended) which at least partially supplements the law on common carriers set forth in the Civil Code. Under Section 13, paragraph (b) of the Public Service Act, "public service" includes: every person that now or hereafter may own, operate. manage, or control in the Philippines, for hire or compensation, with general or limited clientele, whether permanent, occasional or accidental, and done for general business purposes, any common carrier, railroad, street railway, traction railway, subway motor vehicle, either for freight or passenger, or both, with or without fixed route and whatever may be its classification, freight or carrier service of any class, express service, steamboat, or steamship line, pontines, ferries and water craft, engaged in the transportation of passengers or freight or both, shipyard, marine repair shop, wharf or dock, ice plant, ice-refrigeration plant, canal, irrigation system gas, electric light heat and power, water supply and power petroleum, sewerage system, wire or wireless communications systems, wire or wireless broadcasting stations and other similar public services. (De Guzman vs. Court of Appeals, [168 SCRA 617-618, 1988])

Is a carrier under a charter party a common carrier?

Charter party is contract between a shipowner and a merchant, by which a ship is let or hired for the conveyance of goods on a specified voyage, or for a defined period. A vessel might also be chartered to carry passengers on a journey. (Wikipedia)

Generally, private carriage is undertaken by special agreement and the carrier does not hold himself out to carry goods for the general public. The most typical, although not the only form of private carriage, is the charter party, a maritime contract by which the charterer, a party other than the shipowner, obtains the use and service of all or some part of a ship for a period of time or a voyage or voyages. (Hernandez and Peñasales, Philippine Admiralty and Maritime Law, p. p. 243; citing Schoenbaum & Yiannopoulos, p. 364.)

It is a hornbook doctrine that:

In an action against a private carrier for loss of, or injury to, cargo, the burden is on the plaintiff to prove that the carrier was negligent or unseaworthy, and the fact that the goods were lost or damaged while in the carrier's custody does not put the burden of proof on the carrier.

Since . . . a private carrier is not an insurer but undertakes only to exercise due care in the protection of the goods committed to its care, the burden of proving negligence or a breach of that duty rests on plaintiff and proof of loss of, or damage to, cargo while in the carrier's possession does not cast on it the burden of proving proper care and diligence on its part or that the loss occurred from an excepted cause in the contract or bill of lading. However, in discharging the burden of proof, plaintiff is entitled to the benefit of the presumptions and inferences by which the law aids the bailor in an action against a bailee, and since the carrier is in a better position to know the cause of the loss and that it was not one involving its liability, the law requires that it come forward with the information available to it, and its failure to do so warrants an inference or presumption of its liability. However, such inferences and presumptions, while they may affect the burden of coming forward with evidence, do not alter the burden of proof which remains on plaintiff, and, where the carrier comes forward with evidence explaining the loss or damage, the burden of going forward with the evidence is again on plaintiff.

Where the action is based on the shipowner's warranty of seaworthiness, the burden of proving a breach thereof and that such breach was the proximate cause of the damage rests on plaintiff, and proof that the goods were lost or damaged while in the carrier's possession does not cast on it the burden of proving seaworthiness. . . . Where the contract of carriage exempts the carrier from liability for unseaworthiness not discoverable by due diligence, the carrier has the preliminary burden of proving the exercise of due diligence to make the vessel seaworthy. (Vlasons Shipping Inc vs Court of Appeals and National Steel Corporation, G.R. No. 112350 [December 12, 1997])

They are as follows:

- Warranty of Seaworthiness. In every marine insurance upon a ship or freight, or freightage, or upon any thing which is the subject of marine insurance, a warranty is implied that the ship is seaworthy. A ship is seaworthy when reasonably fit to perform the service and to encounter the ordinary perils of the voyage contemplated by the parties to the policy. (Sections 115-116, Insurance Code of the Philippines)

- Warranty that the ship has the documents of neutrality or nationality. Where the nationality or neutrality of a ship or cargo is expressly warranted, it is implied that the ship will carry the requisite documents to show such nationality or neutrality and that it will not carry any documents which cast reasonable suspicion thereon. (Section 122, Insurance Code of the Philippines).

- Warranty against improper deviation. Deviation is a departure from the course of the voyage insured, mentioned in the last two (2) sections, or an unreasonable delay in pursuing the voyage or the commencement of an entirely different voyage.

Define seaworthiness and when is a ship deemed seaworthy?

A ship is seaworthy when reasonably fit to perform the service and to encounter the ordinary perils of the voyage contemplated by the parties to the policy.

An implied warranty of seaworthiness is complied with if the ship be seaworthy at the time of the commencement of the risk, except in the following cases:

- When the insurance is made for a specified length of time, the implied warranty is not complied with unless the ship be seaworthy at the commencement of every voyage it undertakes during that time;

- When the insurance is upon the cargo which, by the terms of the policy, description of the voyage, or established custom of the trade, is to be transhipped at an intermediate port, the implied warranty is not complied with unless each vessel upon which the cargo is shipped, or transhipped, be seaworthy at the commencement of each particular voyage. (Section 116-117, Insurance Code of the Philippines)

When is deviation deemed proper?

It is deemed proper if the following are present:

- When caused by circumstances over which neither the master nor the owner of the ship has any control;

- When necessary to comply with a warranty, or to avoid a peril, whether or not the peril is insured against;

- When made in good faith, and upon reasonable grounds of belief in its necessity to avoid a peril; or

- When made in good faith, for the purpose of saving human life or relieving another vessel in distress. (Section 126, Insurance Code of the Philippines)

Is the warranty of seaworthiness applicable to the cargo owner too aside from the shipowner?

Since the law provides for an implied warranty of seaworthiness in every contract of ordinary marine insurance, it becomes the obligation of a cargo owner to look for a reliable common carrier which keeps its vessels in seaworthy condition. The shipper of cargo may have no control over the vessel but he has full control in the choice of the common carrier that will transport his goods. (Isabela Roque vs Intermediate Appellate Court and Pioneer Insurance and Surety Corporation, (G.R. No. L-66935 November 11, 1985)

Who are the parties in the Marine Adventure?

- Arrastre Operator - the entity engaged in the operation of receiving, conveying, and loading or unloading merchandise on piers or wharves.

- Bailee - the entity to whom the goods are entrusted such as the carrier, warehouseman and trucker. They have insurable interest in the goods insofar as their liability in concerned while the goods are in their possession.

- Shipper - the consignor, the seller or sender of goods.

- Consignee - the person to whom the goods are consigned or entrusted for it to be sold.

- Carrier - the entity who carries the insured goods by air, land or sea.

- Charterer - the entity who hires the vessel for a specific period of time or voyage.

- Trucker - the entity who carries the insured goods by land.

- Freight forwarder - also known as a non-vessel operating common carrier (NVOCC), is a person or company that organizes shipments to get goods from the shipper to a final point of distribution.

- Salvor - the entity who is engaged in saving ship that sunk including the cargo therein.

- Adjuster - the entity assigned to investigate the facts and circumstances surrounding a claim. Some have a specialization like in the case of Average Adjuster who is specialize on general average adjustment claims.

What is a common carrier?

Common carriers are persons, corporations, firms or associations engaged in the business of carrying or transporting passengers or goods or both, by land, water, or air, for compensation, offering their services to the public.

Common carriers, from the nature of their business and for reasons of public policy, are bound to observe extraordinary diligence in the vigilance over the goods and for the safety of the passengers transported by them, according to all the circumstances of each case.

What is the test for determining whether a party is a common carrier of goods or not?

The following elements must be satisfied:

- He must be engaged in the business of carrying goods for others as a public employment, and must hold himself out as ready to engage in the transportation of goods for person generally as a business and not as a casual occupation;

- He must undertake to carry goods of the kind to which his business is confined;

- He must undertake to carry by the method by which his business is conducted and over his established roads; and

- The transportation must be for hire. (First Philippine Industrial Corporation vs Court of Appeals, [G.R. No. 125948 December 29, 1998] citing Agbayani, Commercial Laws of the Phil., 1983 Ed., Vol. 4, p. 5.)

Will the fact that petitioner has a limited clientele does not exclude it from the definition of a common carrier?

Art. 1732 of the Civil Code makes no distinction between one whose principal business activity is the carrying of persons or goods or both, and one who does such carrying only as an ancillary activity (in local idiom, as a "sideline"). Article 1732 . . . avoids making any distinction between a person or enterprise offering transportation service on a regular or scheduled basis and one offering such service on an occasional, episodic or unscheduled basis. Neither does Article 1732 distinguish between a carrier offering its services to the "general public," i.e., the general community or population, and one who offers services or solicits business only from a narrow segment of the general population. We think that Article 1877 deliberately refrained from making such distinctions.

The concept of "common carrier" under Article 1732 may be seen to coincide neatly with the notion of "public service," under the Public Service Act (Commonwealth Act No. 1416, as amended) which at least partially supplements the law on common carriers set forth in the Civil Code. Under Section 13, paragraph (b) of the Public Service Act, "public service" includes: every person that now or hereafter may own, operate. manage, or control in the Philippines, for hire or compensation, with general or limited clientele, whether permanent, occasional or accidental, and done for general business purposes, any common carrier, railroad, street railway, traction railway, subway motor vehicle, either for freight or passenger, or both, with or without fixed route and whatever may be its classification, freight or carrier service of any class, express service, steamboat, or steamship line, pontines, ferries and water craft, engaged in the transportation of passengers or freight or both, shipyard, marine repair shop, wharf or dock, ice plant, ice-refrigeration plant, canal, irrigation system gas, electric light heat and power, water supply and power petroleum, sewerage system, wire or wireless communications systems, wire or wireless broadcasting stations and other similar public services. (De Guzman vs. Court of Appeals, [168 SCRA 617-618, 1988])

Is a carrier under a charter party a common carrier?

Charter party is contract between a shipowner and a merchant, by which a ship is let or hired for the conveyance of goods on a specified voyage, or for a defined period. A vessel might also be chartered to carry passengers on a journey. (Wikipedia)

Generally, private carriage is undertaken by special agreement and the carrier does not hold himself out to carry goods for the general public. The most typical, although not the only form of private carriage, is the charter party, a maritime contract by which the charterer, a party other than the shipowner, obtains the use and service of all or some part of a ship for a period of time or a voyage or voyages. (Hernandez and Peñasales, Philippine Admiralty and Maritime Law, p. p. 243; citing Schoenbaum & Yiannopoulos, p. 364.)

It is a hornbook doctrine that:

In an action against a private carrier for loss of, or injury to, cargo, the burden is on the plaintiff to prove that the carrier was negligent or unseaworthy, and the fact that the goods were lost or damaged while in the carrier's custody does not put the burden of proof on the carrier.

Since . . . a private carrier is not an insurer but undertakes only to exercise due care in the protection of the goods committed to its care, the burden of proving negligence or a breach of that duty rests on plaintiff and proof of loss of, or damage to, cargo while in the carrier's possession does not cast on it the burden of proving proper care and diligence on its part or that the loss occurred from an excepted cause in the contract or bill of lading. However, in discharging the burden of proof, plaintiff is entitled to the benefit of the presumptions and inferences by which the law aids the bailor in an action against a bailee, and since the carrier is in a better position to know the cause of the loss and that it was not one involving its liability, the law requires that it come forward with the information available to it, and its failure to do so warrants an inference or presumption of its liability. However, such inferences and presumptions, while they may affect the burden of coming forward with evidence, do not alter the burden of proof which remains on plaintiff, and, where the carrier comes forward with evidence explaining the loss or damage, the burden of going forward with the evidence is again on plaintiff.

Where the action is based on the shipowner's warranty of seaworthiness, the burden of proving a breach thereof and that such breach was the proximate cause of the damage rests on plaintiff, and proof that the goods were lost or damaged while in the carrier's possession does not cast on it the burden of proving seaworthiness. . . . Where the contract of carriage exempts the carrier from liability for unseaworthiness not discoverable by due diligence, the carrier has the preliminary burden of proving the exercise of due diligence to make the vessel seaworthy. (Vlasons Shipping Inc vs Court of Appeals and National Steel Corporation, G.R. No. 112350 [December 12, 1997])

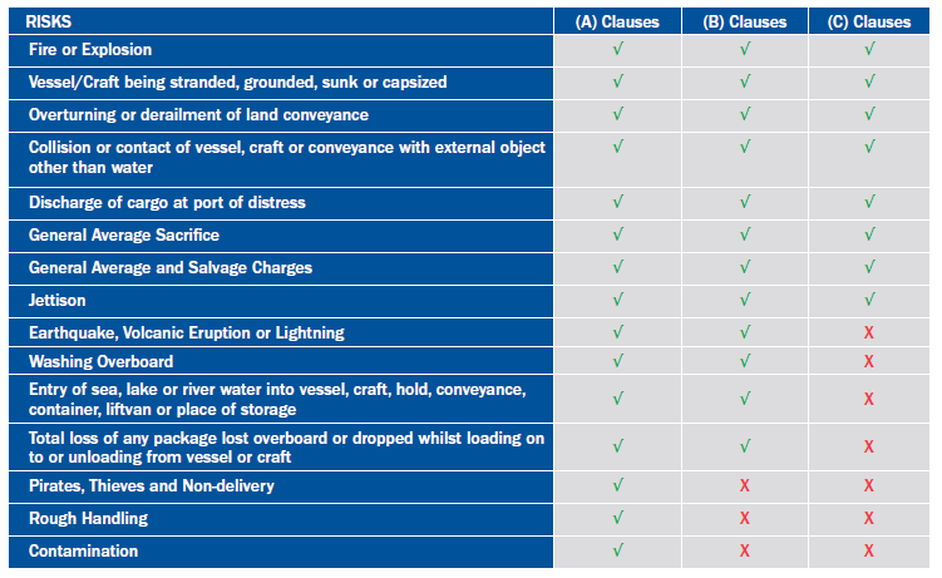

INSTITUTE CARGO CLAUSES

Enumerate the 3 Institute Cargo Clauses and their difference in terms of cover?

There are 3 main cargo clauses in international transactions, namely: Institute Cargo Clauses A, B and C.

Institute Cargo Clause A is the broadest and is also known as an all-risk policy while Institute Cargo Clause C offers the least protection.

There are 3 main cargo clauses in international transactions, namely: Institute Cargo Clauses A, B and C.

Institute Cargo Clause A is the broadest and is also known as an all-risk policy while Institute Cargo Clause C offers the least protection.

Source: AXA Corporate Solutions' Website

Institute Cargo Clause A is also known as an "All Risk" Policy, what is meant by that?

An “all risks” policy of marine insurance is always subject to two limits; first, the coverage afforded by an “all risks” policy has always been subject to the rule of federal admiralty law that only “fortuitous” losses are covered, since if not fortuitous, a loss is not covered by an “all risks” policy of marine insurance, even if not specifically excluded; second, even if a loss is deemed to have been fortuitous, the coverage afforded by an “all risks” policy is narrowed by the policy’s exclusions, which expressly carve out from coverage certain specified losses. (Michael I. Goldman, Esq. The Fortuity Rule of Federal Maritime Law: The Scope of “All Risks” Coverage Under Policies of Marine Insurance and the New Decision of the Eleventh Circuit Court of Appeals. Journal of Maritime Law & Commerce, Vol. 46, No. 2, April, 2015)

What are the variations of Institute Cargo Clauses based on the types of risk covered?

What is grounding?

Grounding is when a ship strikes the seabed. It is commonly referred to as "running aground."

What is stranding?

Stranding is when the ship is stuck or stationery for some length of time due to a fortuitous event. It does not include being stuck as a consequence of the normal rise and fall of the tide.

What is meant by capsized?

It means that the ship or craft is upset or turned over.

What is meant by sunk?

It means that the ship or craft is already lying at the bottom of the body of water.

What is collision?

It is also known as running down. It refers to collision of the insured ship with another ship. Collision with a fixed object, on the other hand, is known as "allision"

What is port of distress?

Refer to a port wherein the ship is forced to unload the cargo which is other than the one she is supposed to dock in order to ensure the safety of the cargo.

What is general average?

It is a contribution by the several interests engaged in the maritime venture to make good the loss of one of them for the voluntary sacrifice of a part of the ship or cargo to save the residue of the property and the lives of those on board, or for extraordinary expenses necessarily incurred for the common benefit and safety of all (California Canneries Co. v. Canton Ins. Office 25 Cal. App. 303, 143 p. 549-553).

The following are the requisites of a General Average:

1. There must be common danger

2. For the common safety, part of the vessel or of the cargo or both is sacrificed deliberately.

3. From the expenses and damages caused follows the successful saving of the vessel and cargo

4. The expenses of damages should have been incurred or inflicted after taking proper legal steps and authority. (A Magsaysay, Inc vs Agan, 96 Phil 504)

What is jettison?

It is the intentional throwing overboard of part of the cargo or some piece of the ship in order to save the ship or its cargo.

What is washing overboard?

Washing overboard is the accidental loss of equipment or cargo overboard due to the action of the elements.

What is piracy?

The term “pirates” includes passengers who mutiny and rioters who attack the ship from the shore. (Rule for the Construction of Policy Number 8 in schedule 1 of the Marine Insurance Act).

What is theft?

The intention is to cover losses wherein there is presence of violence. However, this is a misnomer because theft, under Revised Penal Code of the Philippines, refers to any act of stealing not involving use of intimidation or violence against person or use of force upon things.

What is non-delivery?

It refers to cases wherein the entire cargo, not just a portion thereof, mysteriously disappears in transit without a trace, as opposed to short delivery which involves failure to deliver only a portion of the packages.

What is barratry?

It is the willful misconduct on the part of the master or crew in pursuance of some unlawful or fraudulent purpose without the consent of the owners, and to the prejudice of the owner's interest. Barratry requires a willful and intentional act in its commission. No honest error or judgement or mere negligence, unless criminally gross, can be barratry.

What is pilferage?

Stealing of a few pieces or a small quantity of a relatively large shipment.

An “all risks” policy of marine insurance is always subject to two limits; first, the coverage afforded by an “all risks” policy has always been subject to the rule of federal admiralty law that only “fortuitous” losses are covered, since if not fortuitous, a loss is not covered by an “all risks” policy of marine insurance, even if not specifically excluded; second, even if a loss is deemed to have been fortuitous, the coverage afforded by an “all risks” policy is narrowed by the policy’s exclusions, which expressly carve out from coverage certain specified losses. (Michael I. Goldman, Esq. The Fortuity Rule of Federal Maritime Law: The Scope of “All Risks” Coverage Under Policies of Marine Insurance and the New Decision of the Eleventh Circuit Court of Appeals. Journal of Maritime Law & Commerce, Vol. 46, No. 2, April, 2015)

What are the variations of Institute Cargo Clauses based on the types of risk covered?

- Institute Frozen Meat (A) (not suitable for chilled, cooled or fresh meat)

- Institute Frozen Meat (A) - 24 Hours Breakdown (not suitable for chilled, cooled or fresh meat)

- Institute Frozen Food (A) (Excluding Frozen Meat)

- Institute Frozen Food (B) (Excluding Frozen Meat)

- Institute Bulk Oil Clauses

- Institute Timber Trade Federation Clauses

- Institute Jute Clauses

- Institute Natural Rubber Clauses

What is grounding?

Grounding is when a ship strikes the seabed. It is commonly referred to as "running aground."

What is stranding?

Stranding is when the ship is stuck or stationery for some length of time due to a fortuitous event. It does not include being stuck as a consequence of the normal rise and fall of the tide.

What is meant by capsized?

It means that the ship or craft is upset or turned over.

What is meant by sunk?

It means that the ship or craft is already lying at the bottom of the body of water.

What is collision?

It is also known as running down. It refers to collision of the insured ship with another ship. Collision with a fixed object, on the other hand, is known as "allision"

What is port of distress?

Refer to a port wherein the ship is forced to unload the cargo which is other than the one she is supposed to dock in order to ensure the safety of the cargo.

What is general average?

It is a contribution by the several interests engaged in the maritime venture to make good the loss of one of them for the voluntary sacrifice of a part of the ship or cargo to save the residue of the property and the lives of those on board, or for extraordinary expenses necessarily incurred for the common benefit and safety of all (California Canneries Co. v. Canton Ins. Office 25 Cal. App. 303, 143 p. 549-553).

The following are the requisites of a General Average:

1. There must be common danger

2. For the common safety, part of the vessel or of the cargo or both is sacrificed deliberately.

3. From the expenses and damages caused follows the successful saving of the vessel and cargo

4. The expenses of damages should have been incurred or inflicted after taking proper legal steps and authority. (A Magsaysay, Inc vs Agan, 96 Phil 504)

What is jettison?

It is the intentional throwing overboard of part of the cargo or some piece of the ship in order to save the ship or its cargo.

What is washing overboard?

Washing overboard is the accidental loss of equipment or cargo overboard due to the action of the elements.

What is piracy?

The term “pirates” includes passengers who mutiny and rioters who attack the ship from the shore. (Rule for the Construction of Policy Number 8 in schedule 1 of the Marine Insurance Act).

What is theft?

The intention is to cover losses wherein there is presence of violence. However, this is a misnomer because theft, under Revised Penal Code of the Philippines, refers to any act of stealing not involving use of intimidation or violence against person or use of force upon things.

What is non-delivery?

It refers to cases wherein the entire cargo, not just a portion thereof, mysteriously disappears in transit without a trace, as opposed to short delivery which involves failure to deliver only a portion of the packages.

What is barratry?

It is the willful misconduct on the part of the master or crew in pursuance of some unlawful or fraudulent purpose without the consent of the owners, and to the prejudice of the owner's interest. Barratry requires a willful and intentional act in its commission. No honest error or judgement or mere negligence, unless criminally gross, can be barratry.

What is pilferage?

Stealing of a few pieces or a small quantity of a relatively large shipment.

CLAIMS

What are the elements of a compensable marine claim?

The term ‘All Risks’, although very wide, does have limitations. It does not mean that all loss or damage, however it occurs, is covered. ‘All Risks’ covers things that happen unexpectedly or by accident or by chance (ie fortuitous damage). It does not cover things that are inevitable or almost certain to happen or things that it would be within the control of the Assured to prevent. (Lloyds Agency Department. Cargo Claims and Recoveries Module 3, Retrieved from www.lloyds.com/agency/training)

The transit clause provides for when the marine adventure will commence and when it will terminate.

Under ICC Clauses 1/1/82, the transit shall commence once the insured cargo leaves the warehouse. Cover does not extend to temporary storage prior to transit on vehicles or to such storage in holding areas within a warehouse.

It shall terminate upon the happening of the following:

The cover shall therefore terminate after the expiry of 60 regardless of whether the cargo arrived the insured's final warehouse.

What are the types of losses in Marine Insurance?

There are 3 kinds of losses and they are as follows:

What is abandonment?

Abandonment is the act of the insured by which, after a constructive total loss, he declares the relinquishment to the insurer of his interest in the thing insured. It must satisfy the following:

RC Corporation purchased rice from Thailand, which it intended to sell locally. Due to stormy weather, the ship carrying the rice became submerged in sea water, and with it the rice cargo. When the cargo arrived in Manila, RC filed a claim for total loss with the insurer, because the rice was no longer fit for human consumption. Admittedly, the rice could still be used as animal feed. Is RC’s claim for total loss justified? Explain.

Yes, RC’s claim for total loss is justified. The rice, which was imported from Thailand for sale locally, is obviously intended for consumption by the public. The complete physical destruction of the rice is not essential to constitute an actual total loss. Such a loss exists in this case since the rice, having been soaked in sea water and thereby rendered unfit for human consumption, has become totally useless for the purpose for which it was imported (Pan Malayan Ins Co vs CA GR No. 95070 [Sep 5, 1991])

An insurance company issued a marine insurance policy covering a shipment by sea from Mindoro to Batangas of 1,000 pieces of Mindoro garden stones against “total loss only.” The stones were loaded in two lighters, the first with 600 pieces and the second with 400 pieces. Because of rough seas, damage was caused the second lighter resulting in the loss of 325 out of the 400 pieces. The owner of the shipment filed claims against the insurance company on the ground of constructive total loss inasmuch as more than ¾ of the value of the stones had been lost in one of the lighters. Is the insurance company liable under its policy? Why? (1992 Bar Exams)

The insurance company is not liable under its policy covering against “total loss only” the shipment of 1,000 pieces of Mindoro garden stones. While the same was carried in two barges, it was insured under a single policy. There is no constructive total loss that can claimed since the ¾ rule is to be computed on the total 1,000 pieces of Mindoro garden. The loss of 325 pieces of garden stones is definitely less than 3/4 of 1,000 pieces of garden stones. (Section 139, Insurance Code, cited in Oriental Assurance v. Court of Appeals and Panama Saw Mill, G.R. No. 94052 [August 9, 1991])

M/V Pearly Shells, a passenger and cargo vessel, was insured for P40,000,000.00 against “constructive total loss.” Due to a typhoon, it sank near Palawan. Luckily, there were no casualties, only injured passengers. The ship owner sent a notice of abandonment of his interest over the vessel to the insurance company which then hired professionals to afloat the vessel for P900,000.00. When re-floated, the vessel needed repairs estimated at P2,000,000.00. The insurance company refused to pay the claim of the ship owner, stating that there was “no constructive total loss.”

a) Was there “constructive total loss” to entitle the ship owner to recover from the insurance company? Explain.

No, there was no "constructive total loss" because the vessel was refloated and the costs of refloating plus the needed repairs (P 2.9 Million) will not be more than three-fourths of the value of the vessel. A constructive total loss is one which gives to a person insured a right to abandon. (Sec, 131, Insurance Code) There would have been a constructive total loss had the vessel MN Pearly Shells suffer loss or needed refloating and repairs of more than the required three-fourths of its value, i.e., more than P30.0 Million. (Sec. 139, Insurance Code, cited in Oriental Assurance v. Court of Appeals and Panama Saw Mill, G.R. No. 94052 [August 9, 1991])

However, the insurance company shall pay for the total costs of refloating and needed repairs (P2.9 Million).

b) Was it proper for the ship owner to send a notice of abandonment to the insurance company? Explain.

No, it was not proper for the ship owner to send a notice of abandonment to the insurance company because abandonment can only be availed of when, in a marine insurance contract, the amount to be expended to recover the vessel would have been more than three-fourths of its value. Vessel MN Pearly Shells needed only P2.9 Million, which does not meet the required three-fourths of its value to merit abandonment. (Section 139, Insurance Code, cited in Oriental Assurance v. Court of Appeals and Panama Saw Mill, G.R. No. 94052 [August 9, 1991])

What is deviation in marine insurance policy? (1985 Bar Exams)

Deviation is departure of the vessel from the course of voyage, or unreasonable delay in pursuing the voyage or the commencement of an entirely different voyage.

If the deviation is proper, the contract remains valid. If improper, the insurer is not liable.

A deviation is proper in the following cases:

T, the captain of MV Don Alan, while asleep in his cabin, dreamt of an Intensity 8 earthquake along the path of his ship. On waking up, he immediately ordered the ship to return to port. True enough, the earthquake and tsunami struck three days later and his ship was saved. Was the deviation proper?

(A) Yes, because the deviation was made in good faith and on a reasonable ground for believing that it was necessary to avoid a peril.

(B) No, because no reasonable ground for avoiding a peril existed at the time of the deviation.

(C) No, because T relied merely on his supposed gift of prophecy.

(D) Yes, because the deviation took place based on a reasonable belief of the captain.

- The cause of the loss is covered peril or in case of all risk policy, it is not expressly excluded by the policy.

- The loss is due to a fortuitous event.

- The loss happened during the covered transit period.

The term ‘All Risks’, although very wide, does have limitations. It does not mean that all loss or damage, however it occurs, is covered. ‘All Risks’ covers things that happen unexpectedly or by accident or by chance (ie fortuitous damage). It does not cover things that are inevitable or almost certain to happen or things that it would be within the control of the Assured to prevent. (Lloyds Agency Department. Cargo Claims and Recoveries Module 3, Retrieved from www.lloyds.com/agency/training)

The transit clause provides for when the marine adventure will commence and when it will terminate.

Under ICC Clauses 1/1/82, the transit shall commence once the insured cargo leaves the warehouse. Cover does not extend to temporary storage prior to transit on vehicles or to such storage in holding areas within a warehouse.

It shall terminate upon the happening of the following:

- On delivery to the Consignees' or other final warehouse or place of storage at the destination named herein. Once the lorry or container carrying the goods had arrived at the insured’s final warehouse, the insured transit shall cease. If the goods were damaged during unloading, the insured would not be able to recover under the marine policy as the risk would already have terminated. Under the 1/1/09 version of this clause, the transit period is extended and ceases only on completion of unloading from the carrying vehicle at the final destination. (Lloyds Agency Department. Cargo Claims and Recoveries Module 3, Retrieved from www.lloyds.com/agency/training)

- On delivery to any other warehouse or place of storage, whether prior to or at the destination named herein, which the Assured elect to use either (a) for storage other than in the ordinary course of transit or (b) for allocation or distribution, or

- On the expiry of 60 days after completion of discharge overside of the goods hereby insured from the oversea vessel at the final port of discharge,

The cover shall therefore terminate after the expiry of 60 regardless of whether the cargo arrived the insured's final warehouse.

What are the types of losses in Marine Insurance?

There are 3 kinds of losses and they are as follows:

- Partial Loss - Funny but this is true. The law defines it in this manner - "Every loss which is not total is partial." (Section 130, Insurance Code of the Philippines)

- Constructive Total Loss - A person insured by a contract of marine insurance may abandon the thing insured, or any particular portion thereof separately valued by the policy, or otherwise separately insured, and recover for a total loss thereof, when the cause of the loss is a peril insured against: (a) If more than three-fourths (¾) thereof in value is actually lost, or would have to be expended to recover it from the peril; b) If it is injured to such an extent as to reduce its value more than three-fourths (¾); (c) If the thing insured is a ship, and the contemplated voyage cannot be lawfully performed without incurring either an expense to the insured of more than three-fourths (¾) the value of the thing abandoned or a risk which a prudent man would not take under the circumstances; or (d) If the thing insured, being cargo or freightage, and the voyage cannot be performed, nor another ship procured by the master, within a reasonable time and with reasonable diligence, to forward the cargo, without incurring the like expense or risk mentioned in the preceding subparagraph. But freightage cannot in any case be abandoned unless the ship is also abandoned.

- Actual Total Loss - is caused by:

(a) A total destruction of the thing insured;

(b) The irretrievable loss of the thing by sinking, or by being broken up;

(c) Any damage to the thing which renders it valueless to the owner for the purpose for which he held it; or

(d) Any other event which effectively deprives the owner of the possession, at the port of destination, of the thing insured. (Section 132, Insurance Code of the Philippines)

What is abandonment?

Abandonment is the act of the insured by which, after a constructive total loss, he declares the relinquishment to the insurer of his interest in the thing insured. It must satisfy the following:

- An abandonment must be made within a reasonable time after receipt of reliable information of the loss, but where the information is of a doubtful character, the insured is entitled to a reasonable time to make inquiry.

- An abandonment must be neither partial nor conditional.

- Abandonment is made by giving notice thereof to the insurer, which may be done orally, or in writing: Provided, That if the notice be done orally, a written notice of such abandonment shall be submitted within seven (7) days from such oral notice.

- A notice of abandonment must be explicit, and must specify the particular cause of the abandonment, but need state only enough to show that there is probable cause therefor, and need not be accompanied with proof of interest or of loss. (Sections 142-146, Insurance Code of the Philippines)

RC Corporation purchased rice from Thailand, which it intended to sell locally. Due to stormy weather, the ship carrying the rice became submerged in sea water, and with it the rice cargo. When the cargo arrived in Manila, RC filed a claim for total loss with the insurer, because the rice was no longer fit for human consumption. Admittedly, the rice could still be used as animal feed. Is RC’s claim for total loss justified? Explain.

Yes, RC’s claim for total loss is justified. The rice, which was imported from Thailand for sale locally, is obviously intended for consumption by the public. The complete physical destruction of the rice is not essential to constitute an actual total loss. Such a loss exists in this case since the rice, having been soaked in sea water and thereby rendered unfit for human consumption, has become totally useless for the purpose for which it was imported (Pan Malayan Ins Co vs CA GR No. 95070 [Sep 5, 1991])

An insurance company issued a marine insurance policy covering a shipment by sea from Mindoro to Batangas of 1,000 pieces of Mindoro garden stones against “total loss only.” The stones were loaded in two lighters, the first with 600 pieces and the second with 400 pieces. Because of rough seas, damage was caused the second lighter resulting in the loss of 325 out of the 400 pieces. The owner of the shipment filed claims against the insurance company on the ground of constructive total loss inasmuch as more than ¾ of the value of the stones had been lost in one of the lighters. Is the insurance company liable under its policy? Why? (1992 Bar Exams)

The insurance company is not liable under its policy covering against “total loss only” the shipment of 1,000 pieces of Mindoro garden stones. While the same was carried in two barges, it was insured under a single policy. There is no constructive total loss that can claimed since the ¾ rule is to be computed on the total 1,000 pieces of Mindoro garden. The loss of 325 pieces of garden stones is definitely less than 3/4 of 1,000 pieces of garden stones. (Section 139, Insurance Code, cited in Oriental Assurance v. Court of Appeals and Panama Saw Mill, G.R. No. 94052 [August 9, 1991])

M/V Pearly Shells, a passenger and cargo vessel, was insured for P40,000,000.00 against “constructive total loss.” Due to a typhoon, it sank near Palawan. Luckily, there were no casualties, only injured passengers. The ship owner sent a notice of abandonment of his interest over the vessel to the insurance company which then hired professionals to afloat the vessel for P900,000.00. When re-floated, the vessel needed repairs estimated at P2,000,000.00. The insurance company refused to pay the claim of the ship owner, stating that there was “no constructive total loss.”

a) Was there “constructive total loss” to entitle the ship owner to recover from the insurance company? Explain.

No, there was no "constructive total loss" because the vessel was refloated and the costs of refloating plus the needed repairs (P 2.9 Million) will not be more than three-fourths of the value of the vessel. A constructive total loss is one which gives to a person insured a right to abandon. (Sec, 131, Insurance Code) There would have been a constructive total loss had the vessel MN Pearly Shells suffer loss or needed refloating and repairs of more than the required three-fourths of its value, i.e., more than P30.0 Million. (Sec. 139, Insurance Code, cited in Oriental Assurance v. Court of Appeals and Panama Saw Mill, G.R. No. 94052 [August 9, 1991])

However, the insurance company shall pay for the total costs of refloating and needed repairs (P2.9 Million).

b) Was it proper for the ship owner to send a notice of abandonment to the insurance company? Explain.

No, it was not proper for the ship owner to send a notice of abandonment to the insurance company because abandonment can only be availed of when, in a marine insurance contract, the amount to be expended to recover the vessel would have been more than three-fourths of its value. Vessel MN Pearly Shells needed only P2.9 Million, which does not meet the required three-fourths of its value to merit abandonment. (Section 139, Insurance Code, cited in Oriental Assurance v. Court of Appeals and Panama Saw Mill, G.R. No. 94052 [August 9, 1991])

What is deviation in marine insurance policy? (1985 Bar Exams)

Deviation is departure of the vessel from the course of voyage, or unreasonable delay in pursuing the voyage or the commencement of an entirely different voyage.

If the deviation is proper, the contract remains valid. If improper, the insurer is not liable.

A deviation is proper in the following cases:

- If due to circumstances outside of the control of the captain or shipowner

- If done to comply with warranty

- If made in good faith to avoid a peril

- If made to save human life or another distressed vessel (Jorge Miravite, Bar Review Materials in Commercial Law, 1998 Edition, p183-184)

T, the captain of MV Don Alan, while asleep in his cabin, dreamt of an Intensity 8 earthquake along the path of his ship. On waking up, he immediately ordered the ship to return to port. True enough, the earthquake and tsunami struck three days later and his ship was saved. Was the deviation proper?

(A) Yes, because the deviation was made in good faith and on a reasonable ground for believing that it was necessary to avoid a peril.

(B) No, because no reasonable ground for avoiding a peril existed at the time of the deviation.

(C) No, because T relied merely on his supposed gift of prophecy.

(D) Yes, because the deviation took place based on a reasonable belief of the captain.

What are the standard exclusions under the Institute Cargo Clauses A to C?

They are as follows:

They are as follows:

- loss, damage or expense attributable to wilful misconduct of the Assured. This is a standard exclusion for all types on insurance.

- loss due to ordinary leakage, ordinary loss in weight or volume, or ordinary wear and tear of the subject-matter insured.

- loss, damage or expense caused by insufficiency or unsuitability of packing or preparation of the subject-matter insured. Under the 1/1/2009, the term servant is replaced with employees. It like clarified that employees does not include independent contractors. This exclusion will apply only when the following are present:

- the packing or preparation is carried out by the insured or their employees or

- the packing or preparation is carried out prior to attachment of the risk. - loss, damage or expense caused by inherent vice or nature of the subject-matter insured. Inherent vice refers to the natural condition or characteristics of the insured cargo. For example, fresh fruit will naturally decay over a period of time and iron based metals will oxidize and rust. It means the risk of deterioration of the goods shipped as a result of their natural behaviour in the ordinary course of the contemplated voyage without the intervention of any fortuitous external accident or casualty. (Richards Hogg Lindley. Institute Cargo Clause 2009: A Comparison of the 1982 and 2009 Clauses with additional commentary. Retrieved from http://www.charlestaylor.com/media/72243/Institute-Cargo-Clauses-2009.pdf)

- loss, damage or expense proximately caused by delay, even though the delay be caused by a risk insured against.

- loss, damage or expense arising from insolvency or financial default of the owners managers charterers or operators of the vessel. A claim will be denied if, at the time of loading, the Assured was aware or should have been aware that the voyage might be halted by the financial circumstances of the carrier.

- loss, damage or expense arising from the use of any weapon of war employing atomic or nuclear fission and/or fusion or other like reaction or radioactive force or matter.

- loss, damage or expense arising from unseaworthiness of vessel or craft, unfitness of vessel craft conveyance container or liftvan for the safe carriage of the subject-matter insured, where the Assured or their servants are privy to such unseaworthiness or unfitness, at the time the subject-matter insured is loaded therein. The exclusion therefore applies only if:

- The assured is privy to (i.e. is aware of) unseaworthiness/unfitness of the vessel or craft at the time of loading.

- The container or conveyance is unfit for the safe carriage of the goods and a) the loading is carried out prior to attachment or b) the loading is carried out by the Assured or their employees and they are privy to that unfitness. - loss, damage or expense due to war civil war revolution rebellion insurrection, or civil strife arising therefrom, or any hostile act by or against a belligerent power

- loss, damage or expense due to capture seizure arrest restraint or detainment (piracy excepted), and the consequences thereof or any attempt thereat

- loss, damage or expense due to derelict mines torpedoes bombs or other derelict weapons of war.

- loss, damage or expense due to or caused by strikers, locked-out workmen, or persons taking part in labor disturbances, riots or civil commotions

- loss, damage or expense due to resulting from strikes, lock-outs, labor disturbances, riots or civil commotions

- loss, damage or expense due to or caused by any terrorist or any person acting from a political motive

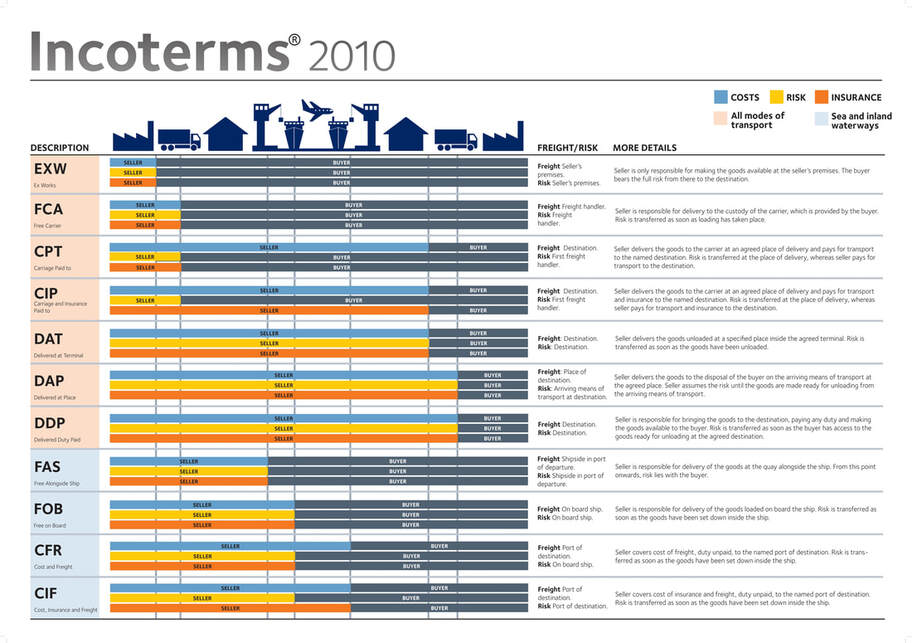

incoterms

What is Incoterms?

It is otherwise known International Commercial Terms. It is a series of pre-defined commercial terms published by the International Chamber of Commerce (ICC) relating to international commercial law.

It refers to terms of sale that determines the following:

It is otherwise known International Commercial Terms. It is a series of pre-defined commercial terms published by the International Chamber of Commerce (ICC) relating to international commercial law.

It refers to terms of sale that determines the following:

- The obligations of the parties

- The point wherein the risk transfers from the seller to the buyer.

Source: http://www.raga-tp.com/index.php/en/const-blog/317-incoterms

Which mode of transport are applicable to Incoterms?

There are main classifications, to wit:

I. Sea transport only

II. All types mode of transport

There are main classifications, to wit:

I. Sea transport only

- FAS

- FOB

- CFR

- CIF

II. All types mode of transport

- EXW

- FCA

- CPT

- CIP

- DAT

- DAP

- DDP

What are the standard claims documents in Marine Insurance

Insurance Policy / Certificate

It serves as an evidence that the cargo has been insured.

Commercial Invoice

The invoice accompanying the consignment, issued by the seller of the goods. This seeks to establish purchase price of goods. It seeks to establish that insurable interest of the claimant.

Packing List

Provides a breakdown of the consignment showing the number of units shipped in each package along with their weights.

Bill of Lading

Has a three-fold nature/function such as: (a) contract of carriage (b) receipt of goods and (c) a document of title that makes it a symbol of the goods.

There are several kinds of Bill of Lading:

The following stipulations in the bill of lading are prohibited:

Air Waybill

Same role as the Bill of Lading but issued by the airline.

Consignment Note

Issued if the goods are carried by road. The consignment note can be signed on delivery and claused to show any damage or shortage in the same way as a road haulier''s Delivery Receipt.

Delivery Receipts

The document signed by the receiver on delivery by the road haulier. As previously mentioned this should be claused to provide evidence of shortage or damage to goods.

Additional Documents

Depending on the circumstances of the claim we may request other documentation such as;

Is the stipulation between the common carrier and the shipper or owner limiting the liability of the former for the loss, destruction, or deterioration of the goods to a degree less than extraordinary diligence valid?

Yes, provided the following must concur:

Is the stipulation that the common carrier's liability is limited to the value of the good appearing in the Bill of Lading valid?

Yes. Unless the shipper or owner declares a greater value. (Article 1749, New Civil Code).

Under COGSA, the shipper can only recover up to US$500 per package unless the value of goods is declared. (Section 4(5), COGSA)

Jacob, the owner of the barge, offered to transport the logs of Essau from Palawan to Manila. Essau accepted the offer not knowing that the barge would be managed by irresponsible crew with deep-seated resentments against Jacob, their employer.

Essau insured his cargo of logs against both perils of the sea and barratry.

The logs were improperly loaded on one side thereby causing the barge to tilt and to navigated on an uneven keel. When the strong winds and high water, normal for the season, started to pound the barge, the crew took advantage of the situation and unbolted the sea valves of the barge causing sea water to come in. The barge sank.

When Essau tried to collect from the insurance firm, the latter stated it could not be held responsible considering the unseaworthiness of both the barge and its crew. Essau countered that he was not the owner of the barge and he could not be held responsible for conditions about which he is innocent.

Is the insurance company liable? Decide with reasons (1986 Bar Exams)

No, the insurance company is not liable. The shipper of the cargo may have no control over the vessel, but he has full control in the choice of the common carrier that will transport his goods. The shipper's choice of the vessel which turns out to be unseaworthy will free the insurer from liability under the insurance contract. (Jorge Miravite, Bar Review Materials in Commercial Law, 1998 Edition, p183)

A shipped 100 pieces of plywood from Davao City to Manila. He took a marine insurance policy to insure the shipment against loss or damage due to "perils of the sea, barratry, fire, jettison, pirates and other such perils"

When the ship left the port of Davao, the shipman in charge forgot to secure on the portholes thru which sea water seeped during the voyage, damaging the plywood. A filed a claim against the insurance company which refused to pay on the ground that the loss was not due to peril of the sea or any of the risk covered under the policy. It was admitted that the sea was reasonably calm during the voyage and that no strong winds or waves were encountered by the vessel.

How would you decide the case? Explain. (1983 Bar Exams)

Recovery under the policy will not prosper. The policy enumerates the perils insured against: perils of the sea, fire, jettison, pirates and other such perils. The last phrase "and other perils" must necessarily have common characteristics as the first five mentioned. Immediately noticeable is that the five does not cover losses due to the fault or negligence of the members of the crew, like the failure to secure one of the portholes of the vessels.

Hence, A cannot recover the damage to his goods from the insurer. (Jorge Miravite, Bar Review Materials in Commercial Law, 1998 Edition, p183-184)

Marine insurance for a sugar shipment was procured by a shipper-consignee on the basis of a sales invoice of the supplier stating that the sugar is in waterproof plastic bags. The insurer, relying on the sales invoice, did not examine the shipment, and issued the covering policy forthwith. Later, the ship carrying the sugar shipment sank at the sea due to a fire of unknown origin. May the shipper-consignee recover on the policy? (1974 Bar Exams)

No, the shipper-consignee may not recover under the marine insurance policy. An ordinary marine insurance policy is an insurance against loss or damage arising from perils of the sea. The fire which burned the cargo is not a peril of the sea. (Jorge Miravite, Bar Review Materials in Commercial Law, 1998 Edition, p183-184)

Insurance Policy / Certificate

It serves as an evidence that the cargo has been insured.

Commercial Invoice

The invoice accompanying the consignment, issued by the seller of the goods. This seeks to establish purchase price of goods. It seeks to establish that insurable interest of the claimant.

Packing List

Provides a breakdown of the consignment showing the number of units shipped in each package along with their weights.

Bill of Lading

Has a three-fold nature/function such as: (a) contract of carriage (b) receipt of goods and (c) a document of title that makes it a symbol of the goods.

There are several kinds of Bill of Lading:

- Clean Bill of Lading – one that does not contain any notation indicating any defect in the goods. An acceptance of the same without objection raises the presumption that all the terms therein were brought to the knowledge of the shipper and agreed to by him. In the absence of fraud or mistake, he is estopped from denying that he assented to such terms. (Magellan Mfg. Marketing Corporation vs Court of Appeal, 201 SCRA 102 (August 22, 1991)

- Foul Bill of Lading – is one that contains a defect or damage to goods

- Custody Bill of Lading – the goods are already received by the carrier but the vessel indicated therein has not yet arrived at the port.

- Port Bill of Lading – under this type, the vessel indicated in the bill of lading that will transport the goods is already at the port.

The following stipulations in the bill of lading are prohibited:

- That the goods are transported at the risk of the owner or shipper;

- That the common carrier will not be liable for any loss, destruction, or deterioration of the goods;

- That the common carrier need not observe any diligence in the custody of the goods;

- That the common carrier shall exercise a degree of diligence less than that of a good father of a family, or of a man of ordinary prudence in the vigilance over the movables transported;

- That the common carrier shall not be responsible for the acts or omission of his or its employees;

- That the common carrier's liability for acts committed by thieves, or of robbers who do not act with grave or irresistible threat, violence or force, is dispensed with or diminished;

- That the common carrier is not responsible for the loss, destruction, or deterioration of goods on account of the defective condition of the car, vehicle, ship, airplane or other equipment used in the contract of carriage (Article 1745, New Civil Code of the Philippines)

Air Waybill

Same role as the Bill of Lading but issued by the airline.

Consignment Note

Issued if the goods are carried by road. The consignment note can be signed on delivery and claused to show any damage or shortage in the same way as a road haulier''s Delivery Receipt.

Delivery Receipts

The document signed by the receiver on delivery by the road haulier. As previously mentioned this should be claused to provide evidence of shortage or damage to goods.

Additional Documents

Depending on the circumstances of the claim we may request other documentation such as;

- Vessel''s Outurn Report

- Container Damage Report

- Tally Sheets

- Written confirmation of Non Delivery from carrier

- Police Statement (in the event of a theft) etc.

- Notice to the carriers.

Is the stipulation between the common carrier and the shipper or owner limiting the liability of the former for the loss, destruction, or deterioration of the goods to a degree less than extraordinary diligence valid?

Yes, provided the following must concur:

- In writing, signed by the shipper or owner;

- Supported by a valuable consideration other than the service rendered by the common carrier; and

- Reasonable, just and not contrary to public policy. (Article 1744, New Civil Code)

Is the stipulation that the common carrier's liability is limited to the value of the good appearing in the Bill of Lading valid?

Yes. Unless the shipper or owner declares a greater value. (Article 1749, New Civil Code).

Under COGSA, the shipper can only recover up to US$500 per package unless the value of goods is declared. (Section 4(5), COGSA)

Jacob, the owner of the barge, offered to transport the logs of Essau from Palawan to Manila. Essau accepted the offer not knowing that the barge would be managed by irresponsible crew with deep-seated resentments against Jacob, their employer.

Essau insured his cargo of logs against both perils of the sea and barratry.

The logs were improperly loaded on one side thereby causing the barge to tilt and to navigated on an uneven keel. When the strong winds and high water, normal for the season, started to pound the barge, the crew took advantage of the situation and unbolted the sea valves of the barge causing sea water to come in. The barge sank.

When Essau tried to collect from the insurance firm, the latter stated it could not be held responsible considering the unseaworthiness of both the barge and its crew. Essau countered that he was not the owner of the barge and he could not be held responsible for conditions about which he is innocent.

Is the insurance company liable? Decide with reasons (1986 Bar Exams)

No, the insurance company is not liable. The shipper of the cargo may have no control over the vessel, but he has full control in the choice of the common carrier that will transport his goods. The shipper's choice of the vessel which turns out to be unseaworthy will free the insurer from liability under the insurance contract. (Jorge Miravite, Bar Review Materials in Commercial Law, 1998 Edition, p183)

A shipped 100 pieces of plywood from Davao City to Manila. He took a marine insurance policy to insure the shipment against loss or damage due to "perils of the sea, barratry, fire, jettison, pirates and other such perils"

When the ship left the port of Davao, the shipman in charge forgot to secure on the portholes thru which sea water seeped during the voyage, damaging the plywood. A filed a claim against the insurance company which refused to pay on the ground that the loss was not due to peril of the sea or any of the risk covered under the policy. It was admitted that the sea was reasonably calm during the voyage and that no strong winds or waves were encountered by the vessel.

How would you decide the case? Explain. (1983 Bar Exams)

Recovery under the policy will not prosper. The policy enumerates the perils insured against: perils of the sea, fire, jettison, pirates and other such perils. The last phrase "and other perils" must necessarily have common characteristics as the first five mentioned. Immediately noticeable is that the five does not cover losses due to the fault or negligence of the members of the crew, like the failure to secure one of the portholes of the vessels.

Hence, A cannot recover the damage to his goods from the insurer. (Jorge Miravite, Bar Review Materials in Commercial Law, 1998 Edition, p183-184)

Marine insurance for a sugar shipment was procured by a shipper-consignee on the basis of a sales invoice of the supplier stating that the sugar is in waterproof plastic bags. The insurer, relying on the sales invoice, did not examine the shipment, and issued the covering policy forthwith. Later, the ship carrying the sugar shipment sank at the sea due to a fire of unknown origin. May the shipper-consignee recover on the policy? (1974 Bar Exams)

No, the shipper-consignee may not recover under the marine insurance policy. An ordinary marine insurance policy is an insurance against loss or damage arising from perils of the sea. The fire which burned the cargo is not a peril of the sea. (Jorge Miravite, Bar Review Materials in Commercial Law, 1998 Edition, p183-184)

RECOVERY

State the deadline to file a claim against the carriers.

The deadline depends on who is the carrier and it shall be as follows:

1. Shipping Line - within 3 days from the time of delivery.

2. Airline - within 14 days from the time of delivery.

3. Road - within 7 days from the time of delivery.

What is the prescription period to file a suit against the carrier and ship under Carriage of Goods by Sea Act (COGSA)?

The prescriptive period is one year from delivery of the goods or the date when the goods should have been delivered. (Section 3(6) of COGSA.

Is there exception to the preceding question?

Yes. In case there is an express agreement between the parties. The agreement shall be the law between them. (Phoenix Assurance Co. Ltd vs United Stated Lines, [22 SCRA 674], Baluyot vs Venegas, [22 SCRA 412], Lazo vs Republic Surety and Insurance Co., Inc., [31 SCRA 329], Philippine American General Insurance Co., Inc vs Mutuc, [61 SCRA 22-23]).

Is the one-year prescription period applicable to insurers as well?

Yes. Otherwise, what COGSA intends to prohibit after the lapse of the one-year prescriptive period can be done indirectly by the shipper or owner by simply filing a claim against the insurer even after the lapse of one year. (Filipino Merchants Insurance Co., Inc vs Hon. Jose Alejandro and Frota Oceanica, [GR No. L-51440, October 14, 1986, Yek Ton Fire and Marine Insurance Co., Ltd vs American President Lines, Inc. [103 Phil 2225-26])

The case applies only if the suit is filed against the carrier either by the shipper, the consignee or the insurer. The prescription shall not apply in case the shipper is pursuing a claim against the insurer. The basis of liability of the insurer is the insurance contract and not the contract of carriage. (See Mayer Steel Pipe Corporation and Hong Kong Government Department vs Court of Appeals, South Sea Surety and Insurance Co., Inc and Charter Insurance Corporation,[274 SCRA 432])

Is the one year prescription period applicable in case of misdelivery or conversion?

No. As a consequence, the prescription period of 10 years shall apply for breach of a written contract or 4 years in case of quasi-delict. (Ang vs. American Steamship Agencies, Inc. [19 SCRA 123]). Loss as contemplated by COGSA refers a situation wherein there is no delivery because the same already perished, gone of out commerce, or disappeared in a way that their existence is unknown or they cannot be recovered. It does not include a situation where there was indeed a delivery – delivery was made to the wrong person. (Domingo Ang vs American Steamship Agencies Inc GR Nos L-25047)

What are the defenses of the common carrier in case of loss, destruction, or deterioration of the goods under their custody?

The deadline depends on who is the carrier and it shall be as follows:

1. Shipping Line - within 3 days from the time of delivery.

2. Airline - within 14 days from the time of delivery.

3. Road - within 7 days from the time of delivery.

What is the prescription period to file a suit against the carrier and ship under Carriage of Goods by Sea Act (COGSA)?

The prescriptive period is one year from delivery of the goods or the date when the goods should have been delivered. (Section 3(6) of COGSA.

Is there exception to the preceding question?

Yes. In case there is an express agreement between the parties. The agreement shall be the law between them. (Phoenix Assurance Co. Ltd vs United Stated Lines, [22 SCRA 674], Baluyot vs Venegas, [22 SCRA 412], Lazo vs Republic Surety and Insurance Co., Inc., [31 SCRA 329], Philippine American General Insurance Co., Inc vs Mutuc, [61 SCRA 22-23]).

Is the one-year prescription period applicable to insurers as well?

Yes. Otherwise, what COGSA intends to prohibit after the lapse of the one-year prescriptive period can be done indirectly by the shipper or owner by simply filing a claim against the insurer even after the lapse of one year. (Filipino Merchants Insurance Co., Inc vs Hon. Jose Alejandro and Frota Oceanica, [GR No. L-51440, October 14, 1986, Yek Ton Fire and Marine Insurance Co., Ltd vs American President Lines, Inc. [103 Phil 2225-26])

The case applies only if the suit is filed against the carrier either by the shipper, the consignee or the insurer. The prescription shall not apply in case the shipper is pursuing a claim against the insurer. The basis of liability of the insurer is the insurance contract and not the contract of carriage. (See Mayer Steel Pipe Corporation and Hong Kong Government Department vs Court of Appeals, South Sea Surety and Insurance Co., Inc and Charter Insurance Corporation,[274 SCRA 432])

Is the one year prescription period applicable in case of misdelivery or conversion?

No. As a consequence, the prescription period of 10 years shall apply for breach of a written contract or 4 years in case of quasi-delict. (Ang vs. American Steamship Agencies, Inc. [19 SCRA 123]). Loss as contemplated by COGSA refers a situation wherein there is no delivery because the same already perished, gone of out commerce, or disappeared in a way that their existence is unknown or they cannot be recovered. It does not include a situation where there was indeed a delivery – delivery was made to the wrong person. (Domingo Ang vs American Steamship Agencies Inc GR Nos L-25047)

What are the defenses of the common carrier in case of loss, destruction, or deterioration of the goods under their custody?

- The common carrier must prove that the loss, destruction, or deterioration of the goods are caused by the following: (a) Flood, storm, earthquake, lightning, or other natural disaster or calamity; (b) Act of the public enemy in war, whether international or civil; (c) Act or omission of the shipper or owner of the goods; (d) The character of the goods or defects in the packing or in the containers; (d) Order or act of competent public authority. (Article 1733, New Civil Code)

- If the goods are lost, destroyed or deteriorated, common carriers by causes outside of the above list, common carrier must prove that they observed extraordinary diligence. Note that common carriers are presumed to have been at fault or to have acted negligently in case of a loss. (Articles 1734, New Civil Code).

THE DATA CONTAINED IN THIS SITE ARE FOR GENERAL INFORMATIONAL PURPOSES ONLY. THE ADVICE OF A PROFESSIONAL INSURANCE INTERMEDIARY AND COUNSEL SHOULD ALWAYS BE OBTAINED.